Following the rally in Pakistan’s global Eurobonds, the country’s risk of default, as measured by credit default swaps (CDS), reached a six-month low of 46.76% last week, following the successful completion of a $3 billion International Monetary Fund (IMF) agreement. This development signifies a substantial restoration of global investors’ confidence in the domestic economy and paves the way for Islamabad to return to international bond markets in the near future in order to raise new debt financing and increase foreign exchange reserves.

During the current fiscal year 2024, the government aims to raise $1.5 billion through the issuance of Eurobonds and/or Sukuk on global markets.

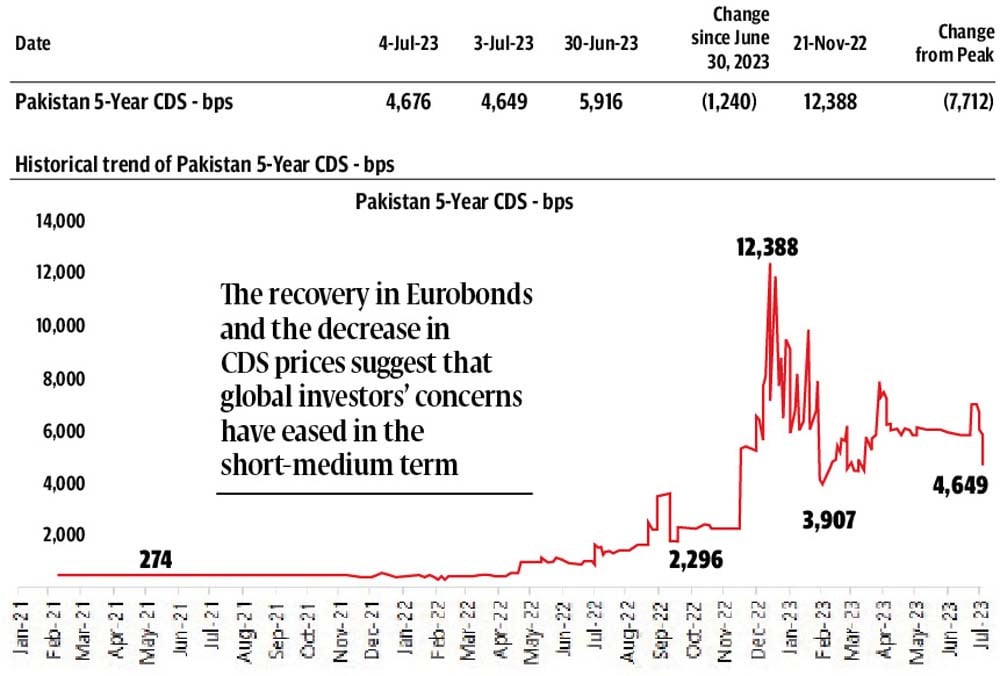

Credit default swaps (CDS) are insurance products that global investors buy to protect themselves from potential losses in the event that a government fails to repay international bonds at maturity.

Tahir Abbas, the head of research at Arif Habib Limited, disclosed that the five-year CDS fell by 12.40 percentage points to 46.76% on Tuesday, following the unexpected completion of the $3 billion IMF agreement on Friday. This represents a significant improvement of 77.12 percentage points over the last eight months, compared to the record high of 123.88% attained on November 21, 2022, when Pakistan’s $6.5 billion loan program derailed and remained stalled until its premature conclusion on June 30, 2023.

Despite this recovery, the 5-year CDS price of 46.76 percent remains elevated compared to the 2.75 percent recorded in March 2021, when the country had stable foreign exchange reserves, as opposed to the current level of $4 billion, which is critically low.

Despite the decline in the risk of default, the Pakistani rupee failed to maintain its gains against the US dollar on Wednesday’s domestic interbank market. This is due to the high demand for foreign currency to clear import backlogs and pay for liberalized imports under the IMF’s program. The rupee fell 0.71 percent, or Rs1.97, to Rs277.41 per dollar on the interbank market on Wednesday, following a significant increase of 3.83 percent on Tuesday.

According to the Exchange Companies Association of Pakistan (ECAP), on the open market the rupee fell by Rs1 to Rs281/$ from Rs280/$ the previous day.

Notable is that Pakistan’s $1 billion 10-year Eurobond, maturing in April 2024, regained 55% of its value following the IMF program rally, reaching an annual high of 80 cents per dollar on Tuesday. Before Pakistan signed the staff level agreement (SLA) with the IMF for the $3 billion loan, the bond was trading at 51.5 cents. The recovery of Eurobonds and the decline in CDS prices suggest that global investors’ concerns regarding Pakistan’s economy have diminished in the short to medium term, corresponding with the three-quarter duration of the current IMF programme.

However, there are a number of other factors that will help the government determine when to return to the international bond markets to raise new funds. This includes the revision of Pakistan’s credit ratings by international rating agencies such as Moody’s and Fitch, which presently rank the nation as junk. In order to secure new funds at favorable terms on the global bond markets, rating upgrades are required. In the next three to six months, rating agencies are expected to reevaluate Pakistan’s creditworthiness in light of the country’s performance under the new IMF agreement.

In addition, the global interest rate scenario and liquidity position will impact Pakistan’s decision regarding when to launch new bonds on global markets, according to Abbas. While it is anticipated that global interest rates will remain elevated in the short term to combat inflation, a rate reversal could increase market liquidity in the long run.

Previously, Pakistan had issued international bonds with a return rate of approximately 7-8%. Abbas stated that Wednesday’s decrease in the value of the Pakistani rupee was merely a correction following Tuesday’s significant decline. He believes that the highly anticipated confirmation of the new $3 billion IMF programme by the Executive Board on July 12 and the first installment of the IMF loan will assist the currency in regaining further ground against the U.S. dollar.

In addition, capital inflows from other global creditors and friendly nations, equal to approximately $3 billion to $4 billion over the course of FY24, are anticipated to continue supporting the rupee. In the immediate term, the currency may stabilize between Rs270 and Rs275 per dollar.